I do not see 2 Dec expiry for SPY. I see SPY weekly expire on 6 Dec. Did you mean SPY 580C exp Dec 6?

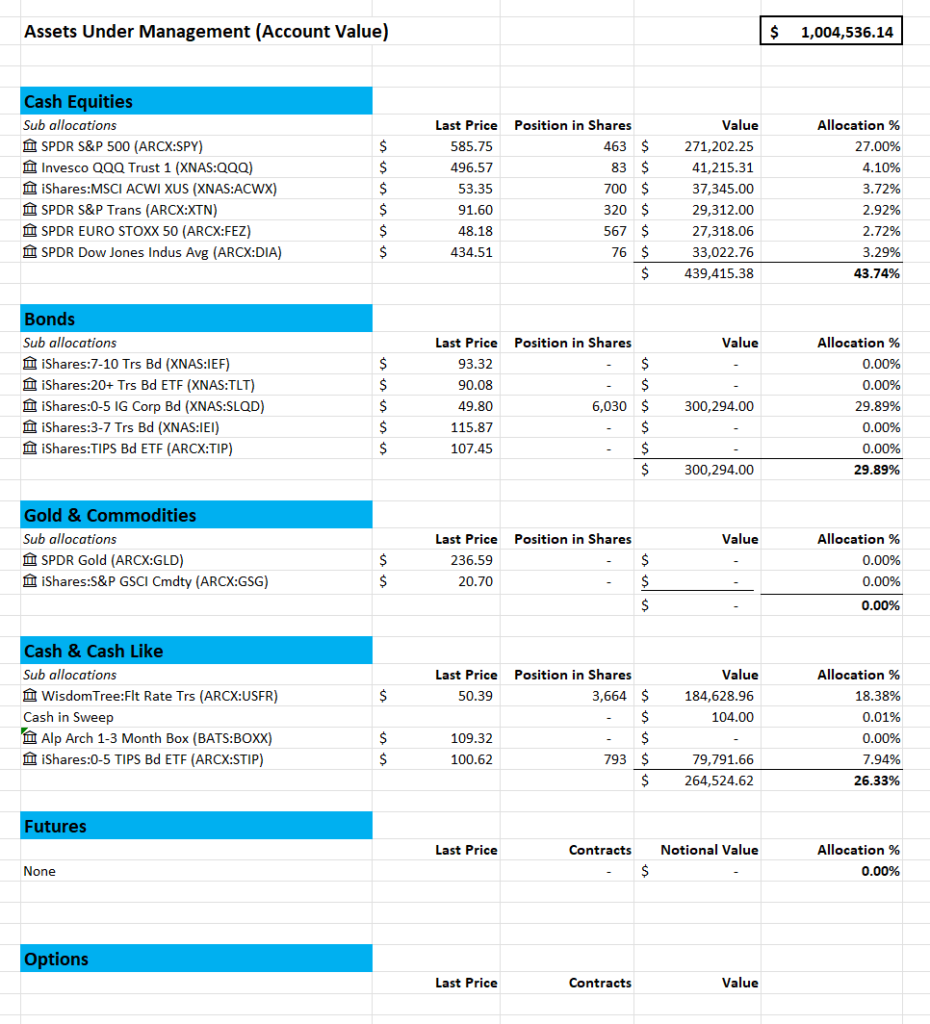

In terms of sizing, we are going about 400K short on SPY, but we do not have 400K SPY in the portfolio. We have other (correlated) equities. What is the view here – are we going short SPY intentionally or do we count our total equities exposure for the purpose of selling these SPY calls?

Sorry for tons of questions, but I want to be careful with this move.

If my understanding on how these options work is correct, one consideration is that the delta of the short calls isn’t -1. In other words, if SPY gains $1 then the options won’t lose $1 in value, but less. The deeper these go ITM, the more delta decreases towards -1 however. Therefore even if we’re selling a notional amount of SPY options (7 * 100 * $580 = $406.000) against our ~$439K total equity position, the emerging market and Europe positions are unlikely to move 1:1 with SPY either. So we’re not net short SPY but rather closer to flat.

No, it was my mistake. Forgot to put it in there. Was going to correct it on Monday morning before open, but decided that the likely price would now be too low after the gold rally. Now, immaterial.

I’d like to pick your thoughts a little so as to learn. During wk 55 in 2gbds original you advised us to do a stock replacement and buy calls when you felt equities would decline. In this instance, you are advising to hold our equities and sell calls. Is this because you have concerns that equities could suddenly move but are less certain about the direction (or perhaps another rationale that I’m completely missing)?

Great question Cathy, I wonder the same. Attempting to answer for my own education. I think the 2GB view is that equities will decline modestly, but not significantly. Therefore they want to dampen any losses by selling in-the-money calls, rather than replace the position altogether.

It also took me a minute to wrap my head around the implications of selling ITM calls. It’d be great if you can touch on the rationale for this, and how we’d manage it in case of them expiring ITM. Would we cover or take the short, going nearly flat equities? Thanks!

This is my personal opinion of course:

– There is not much difference selling ITM or OTM calls till about 2-5 days to expiry. No one would exercise the call till closer to expiry.

– Chances are the call won’t be ITM by Monday open.

All depends on the level of implied volatility, relative to the expected move of the underlying. If I expect a 2% move, why would I pay that to protect myself? I would make nothing even if I was right. When volatility is very low, it naturally pays to hedge via call substitution of stocks, now not so much.

Continuing the lines of thought of Cathy and Ox_brucey, if holding a December 31 or Jan 17 SPY 600 call would one create a calendar spread by selling the nearer term 580 call?

Well, it is a spread and it is a calendar. So, yes. You are betting on a short term pullback to cover the front leg and then a longer term rally after that.

So if they can keep bullin it over these next days, what might you consider a reasonable ‘get out’ level.

And/or how would we approach repairing the trade. Thks.

12 Responses

i might have missed it somehow, but I do not see the expiry for GLD puts in the video. What is the expiry ?

I do not see 2 Dec expiry for SPY. I see SPY weekly expire on 6 Dec. Did you mean SPY 580C exp Dec 6?

In terms of sizing, we are going about 400K short on SPY, but we do not have 400K SPY in the portfolio. We have other (correlated) equities. What is the view here – are we going short SPY intentionally or do we count our total equities exposure for the purpose of selling these SPY calls?

Sorry for tons of questions, but I want to be careful with this move.

I do see the Dec 2nd ’24 expiry in IBKR.

If my understanding on how these options work is correct, one consideration is that the delta of the short calls isn’t -1. In other words, if SPY gains $1 then the options won’t lose $1 in value, but less. The deeper these go ITM, the more delta decreases towards -1 however. Therefore even if we’re selling a notional amount of SPY options (7 * 100 * $580 = $406.000) against our ~$439K total equity position, the emerging market and Europe positions are unlikely to move 1:1 with SPY either. So we’re not net short SPY but rather closer to flat.

Yes, now i see 2Dec SPY expiry. My broker did not have it on the weekend

No, it was my mistake. Forgot to put it in there. Was going to correct it on Monday morning before open, but decided that the likely price would now be too low after the gold rally. Now, immaterial.

I’d like to pick your thoughts a little so as to learn. During wk 55 in 2gbds original you advised us to do a stock replacement and buy calls when you felt equities would decline. In this instance, you are advising to hold our equities and sell calls. Is this because you have concerns that equities could suddenly move but are less certain about the direction (or perhaps another rationale that I’m completely missing)?

Great question Cathy, I wonder the same. Attempting to answer for my own education. I think the 2GB view is that equities will decline modestly, but not significantly. Therefore they want to dampen any losses by selling in-the-money calls, rather than replace the position altogether.

It also took me a minute to wrap my head around the implications of selling ITM calls. It’d be great if you can touch on the rationale for this, and how we’d manage it in case of them expiring ITM. Would we cover or take the short, going nearly flat equities? Thanks!

This is my personal opinion of course:

– There is not much difference selling ITM or OTM calls till about 2-5 days to expiry. No one would exercise the call till closer to expiry.

– Chances are the call won’t be ITM by Monday open.

All depends on the level of implied volatility, relative to the expected move of the underlying. If I expect a 2% move, why would I pay that to protect myself? I would make nothing even if I was right. When volatility is very low, it naturally pays to hedge via call substitution of stocks, now not so much.

Continuing the lines of thought of Cathy and Ox_brucey, if holding a December 31 or Jan 17 SPY 600 call would one create a calendar spread by selling the nearer term 580 call?

Thanks.

Well, it is a spread and it is a calendar. So, yes. You are betting on a short term pullback to cover the front leg and then a longer term rally after that.

So if they can keep bullin it over these next days, what might you consider a reasonable ‘get out’ level.

And/or how would we approach repairing the trade. Thks.