Timestamps What Happened Last Week – 00:23 What’s Happening Next Week – 12:56 Nick’s Update – 17:58

14 Responses

Another great weekly presentation

For the 1MM account would you say that is minimum amount needed in the account or could someone run your strategy with say 7~800K and just scale down the positions.

I would say $500k would be more than enough, with 1/2 allocation, naturally. $500k would be more than enough to cover all position requirements, margins, etc…

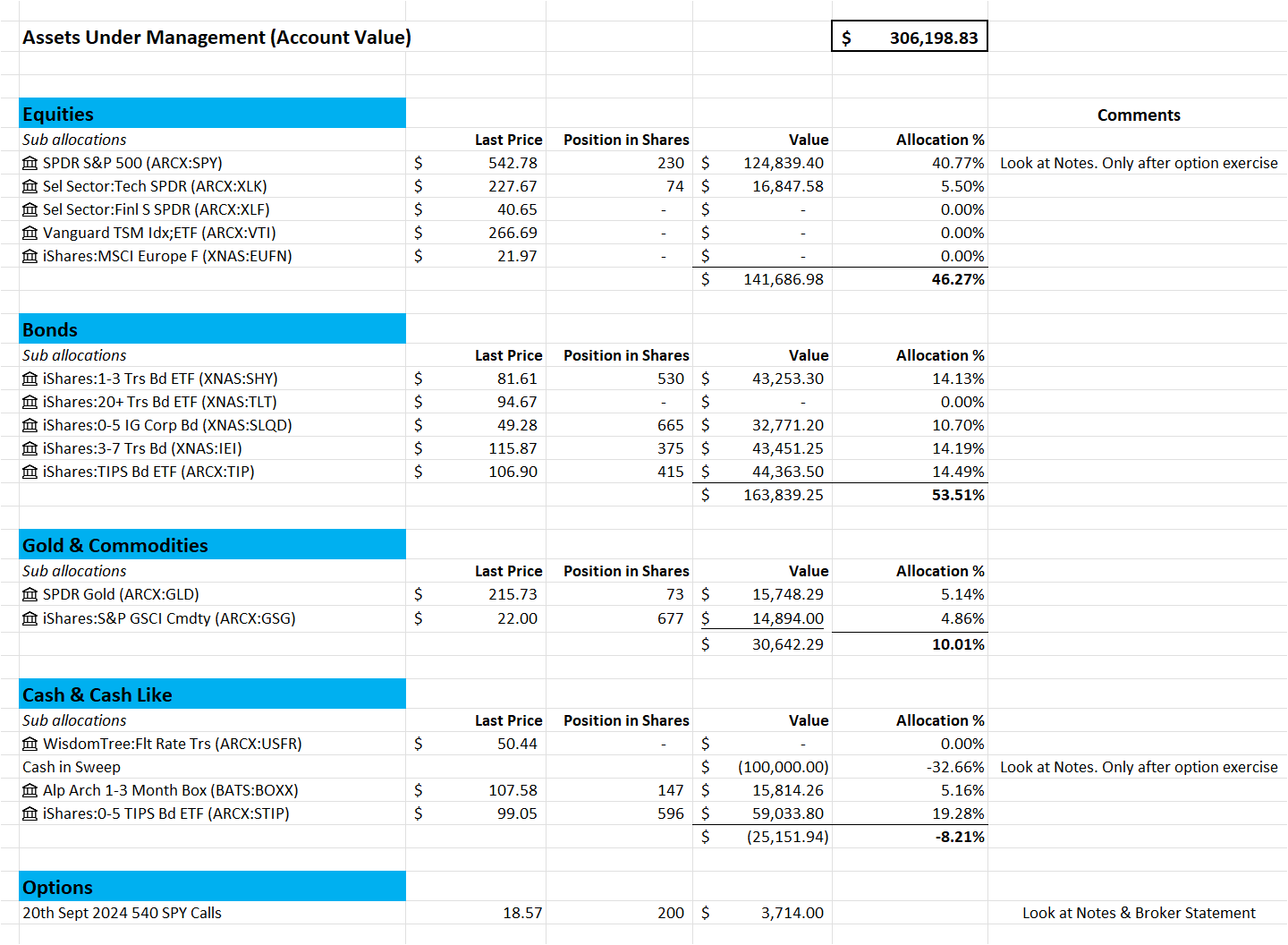

If you notice, with portfolio margining at the moment we are currently using approx. $30k for this account, which is not levered at all, so about 10%. Even if we doubled the overall margining (at times) and NOT NET leverage (IE: using long leveraged call spreads, etc), I doubt we will ever get even close to $100k, so 30% of AUM. But that is with a portfolio margining account, which I would recommend to everyone.

100% of my funds available for 2GB strategies are in Schwab IRA accts.

I have full options approval ex naked calls, and will look to expand to include whatever futures trading Schwab allows.

However, I will obviously never be allowed margin and will be limited by 1-day settlement.

I happily accept that I will be able to implement only a subset of the published trades, confident that subset is still quite superior to my pre-2GB results.

I suspect I am not the only subscriber in this category.

It would be helpful if your trade alerts indicated an “ideal” implementation and, if different and where possible, an “IRA” implementation. Again, I realize the IRA version may be suboptimal (or not possible), but your guidance will be much easier than each of us trying to discern a best alternate trade.

One approach is to buy the put or call that would give the same max cash loss as the margin requirement, turning a naked sell into a spread. That’s what I do in IRAs to simulate margiin on what would be naked sells otherwise. Hurts the return by the cost of the purchased option which can be small.

Yes that would be 1 way around the regulations. If you could not sell a naked put, turn it into a put spread with the lower leg far, far out of the money, therefore costing next to nothing. But the bigger problem in IRAs, as I understand it, and could be totally wrong, is leverage. Say you had $1m in IRA account. Can you buy options with NOMINAL value greater than $1m? Not margin required, but nominal value of options themselves? Can the nominal value be greater than IRA AUM? If you can, then no problems.

great work around

The 1 day settlement is not a problem. It only restricts you to NOT selling whatever you bought that same day. So, if you sell USFR, say, to buy, say, SPX, it prevents you from selling that SPX before the funds settled from USFR. And we never do that. So that is not an issue.

I am not an expert on IRAs. I don’t have one, never have. But it is my understanding that different brokerages have different levels of permissions in their IRAs, concerning naked selling of options, futures trading, etc. And that they define leverage in different ways. I just can’t know all the variants.

A bit of speculation here: I understand how risk off in Europe could hit US equities, but isn’t there a case to be made for a rotation out of Europe into the US – equities? Either way, I’m glad we exited EUFN when we did.

I have traded options in Schwab for close to 20 yrs.

Here is my understanding of Schwab’s boundaries on options positions.

Some of this is SEC and some of it is Schwab – so I assume it is representative of what most IRA accounts encounter.

Bottom line – Schwab requires cash or cash equivalents to meet the potential unilateral obligations of the options holder. There is no margin available to “bridge the gap”

=================================================

LONG OPTIONS – The account needs enough unencumbered cash to pay the option premium.

So, I could have sold out of USFR when you suggested and allocated 100% of the proceeds to $GME 5 delta calls.

In this example, if the stock zooms up and the acct holder chooses to exercise to receive shares, the transaction is limited to cash on hand – the balance of the options must be bought back to close or allowed to expire.

SHORT OPTIONS — The account needs enough unencumbered cash or cash equivalents to meet assignment.

Naked puts: ( strike * qty ) – prem recd <= available CASH or MMF or UST NOTES

Naked calls: Not allowed because the risk to Schwab is indeterminate

CR spread: : ( [ shrt strk – long strk ] * qty ) – prem recd <= available CASH or MMF or UST NOTES

=================================================

I have had positions where the exercise value of open longs plus the assignment value of open shorts exceed the available cash + equlivalents.

As long as I manage to the calcs above, I have had no problems.

It seems this framework offers enough flexibility to mostly mirror what you might suggest.

Looks to me like no problem at all. Or not much that cannot be mitigated with a bit of extra care/attention/ingenuity. Only worry would be if someone does not know all these rules intimately, as presumably you learnt all this over the course of years and mistakes can happen in meantime. Certainly my case, I tend to learn best by screwing up :).

14 Responses

Another great weekly presentation

For the 1MM account would you say that is minimum amount needed in the account or could someone run your strategy with say 7~800K and just scale down the positions.

Thanks again

I would say $500k would be more than enough, with 1/2 allocation, naturally. $500k would be more than enough to cover all position requirements, margins, etc…

If you notice, with portfolio margining at the moment we are currently using approx. $30k for this account, which is not levered at all, so about 10%. Even if we doubled the overall margining (at times) and NOT NET leverage (IE: using long leveraged call spreads, etc), I doubt we will ever get even close to $100k, so 30% of AUM. But that is with a portfolio margining account, which I would recommend to everyone.

Nick…

100% of my funds available for 2GB strategies are in Schwab IRA accts.

I have full options approval ex naked calls, and will look to expand to include whatever futures trading Schwab allows.

However, I will obviously never be allowed margin and will be limited by 1-day settlement.

I happily accept that I will be able to implement only a subset of the published trades, confident that subset is still quite superior to my pre-2GB results.

I suspect I am not the only subscriber in this category.

It would be helpful if your trade alerts indicated an “ideal” implementation and, if different and where possible, an “IRA” implementation. Again, I realize the IRA version may be suboptimal (or not possible), but your guidance will be much easier than each of us trying to discern a best alternate trade.

Thank you.

/MCS

Portland, OR

One approach is to buy the put or call that would give the same max cash loss as the margin requirement, turning a naked sell into a spread. That’s what I do in IRAs to simulate margiin on what would be naked sells otherwise. Hurts the return by the cost of the purchased option which can be small.

Yes that would be 1 way around the regulations. If you could not sell a naked put, turn it into a put spread with the lower leg far, far out of the money, therefore costing next to nothing. But the bigger problem in IRAs, as I understand it, and could be totally wrong, is leverage. Say you had $1m in IRA account. Can you buy options with NOMINAL value greater than $1m? Not margin required, but nominal value of options themselves? Can the nominal value be greater than IRA AUM? If you can, then no problems.

great work around

The 1 day settlement is not a problem. It only restricts you to NOT selling whatever you bought that same day. So, if you sell USFR, say, to buy, say, SPX, it prevents you from selling that SPX before the funds settled from USFR. And we never do that. So that is not an issue.

I am not an expert on IRAs. I don’t have one, never have. But it is my understanding that different brokerages have different levels of permissions in their IRAs, concerning naked selling of options, futures trading, etc. And that they define leverage in different ways. I just can’t know all the variants.

A bit of speculation here: I understand how risk off in Europe could hit US equities, but isn’t there a case to be made for a rotation out of Europe into the US – equities? Either way, I’m glad we exited EUFN when we did.

For sure. It happened on Friday. Likely to continue.

Nick –

I have traded options in Schwab for close to 20 yrs.

Here is my understanding of Schwab’s boundaries on options positions.

Some of this is SEC and some of it is Schwab – so I assume it is representative of what most IRA accounts encounter.

Bottom line – Schwab requires cash or cash equivalents to meet the potential unilateral obligations of the options holder. There is no margin available to “bridge the gap”

=================================================

LONG OPTIONS – The account needs enough unencumbered cash to pay the option premium.

So, I could have sold out of USFR when you suggested and allocated 100% of the proceeds to $GME 5 delta calls.

In this example, if the stock zooms up and the acct holder chooses to exercise to receive shares, the transaction is limited to cash on hand – the balance of the options must be bought back to close or allowed to expire.

SHORT OPTIONS — The account needs enough unencumbered cash or cash equivalents to meet assignment.

Naked puts: ( strike * qty ) – prem recd <= available CASH or MMF or UST NOTES

Naked calls: Not allowed because the risk to Schwab is indeterminate

CR spread: : ( [ shrt strk – long strk ] * qty ) – prem recd <= available CASH or MMF or UST NOTES

=================================================

I have had positions where the exercise value of open longs plus the assignment value of open shorts exceed the available cash + equlivalents.

As long as I manage to the calcs above, I have had no problems.

It seems this framework offers enough flexibility to mostly mirror what you might suggest.

Looks to me like no problem at all. Or not much that cannot be mitigated with a bit of extra care/attention/ingenuity. Only worry would be if someone does not know all these rules intimately, as presumably you learnt all this over the course of years and mistakes can happen in meantime. Certainly my case, I tend to learn best by screwing up :).

Maybe I missed this but is the account transitioning to just the $1mm model portfolio or both the $1mm and 300k?

Both.

Sounds like subscription price may but changing?